What Is a South Carolina Promissory Note?

A South Carolina promissory note is a formal agreement detailing the terms under which a lender loans money to a borrower. This legally binding document explains the loan amount, interest rate, and repayment schedule and describes the consequences of default.

This document ensures both parties understand their obligations and serves as a clear record of the transaction. By specifying conditions for the loan’s repayment and any security the borrower provides (if applicable), the promissory note safeguards the lender’s and borrower’s interests.

Laws: Promissory notes fall under Title 36, Chapter 3 (Negotiable Instruments) of the South Carolina Uniform Commercial Code.

Statute of Limitations: Six years (§ 36-3-118).

Types of South Carolina Promissory Notes: Secured vs. Unsecured

South Carolina lenders should tailor their loan documents to the situation. The right promissory note helps maintain trust while providing the legal backup you need.

Secured South Carolina Promissory Note

Lets the lender retain an asset (such as a car or house) if the borrower doesn't repay their loan.

Unsecured South Carolina Promissory Note

The borrower doesn't need to provide collateral for this loan because they can often seek it with a good credit score.

Usury Laws and Interest Rates in South Carolina

South Carolina’s interest and usury laws fall under Title 34, Chapter 31 (Money and Interest) and Title 37, Chapter 3 (Loans):

-

For Monetary Judgments (§ 34-31-20(B)): For each year a debtor owes damages to a creditor/plaintiff, interest will be calculated with the Wall Street Journal’s published prime rate plus 4% (compounded annually). Here’s what interest rate calculations look like for older judgments:

- 12% a year for judgments entered between January 1, 2001, and June 30, 2005.

- 14% a year for judgments entered before January 1, 2001.

- For Unsupervised Loans (§ 37-3-201(1)): 12%.

- For Supervised Loans (§ 37-3-201(2)(c)): 18%.

- In General (§ 34-31-20(A)): 8.75%.

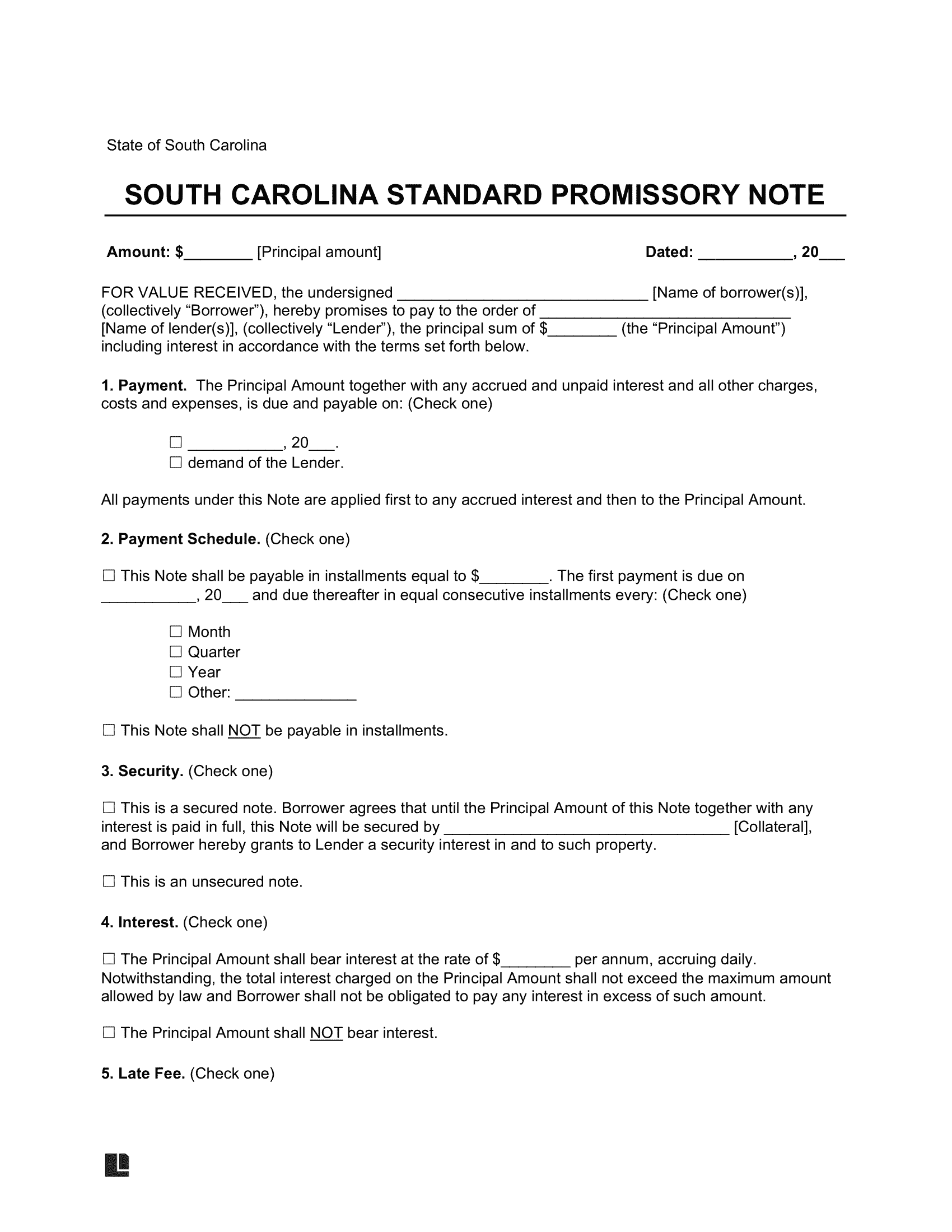

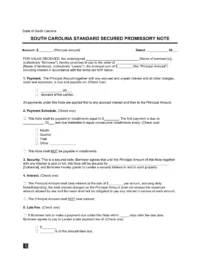

Sample South Carolina Promissory Note

View a free example South Carolina promissory note to see its structure. When you’re ready, create your own via our document editor and download it as a PDF or Word file.