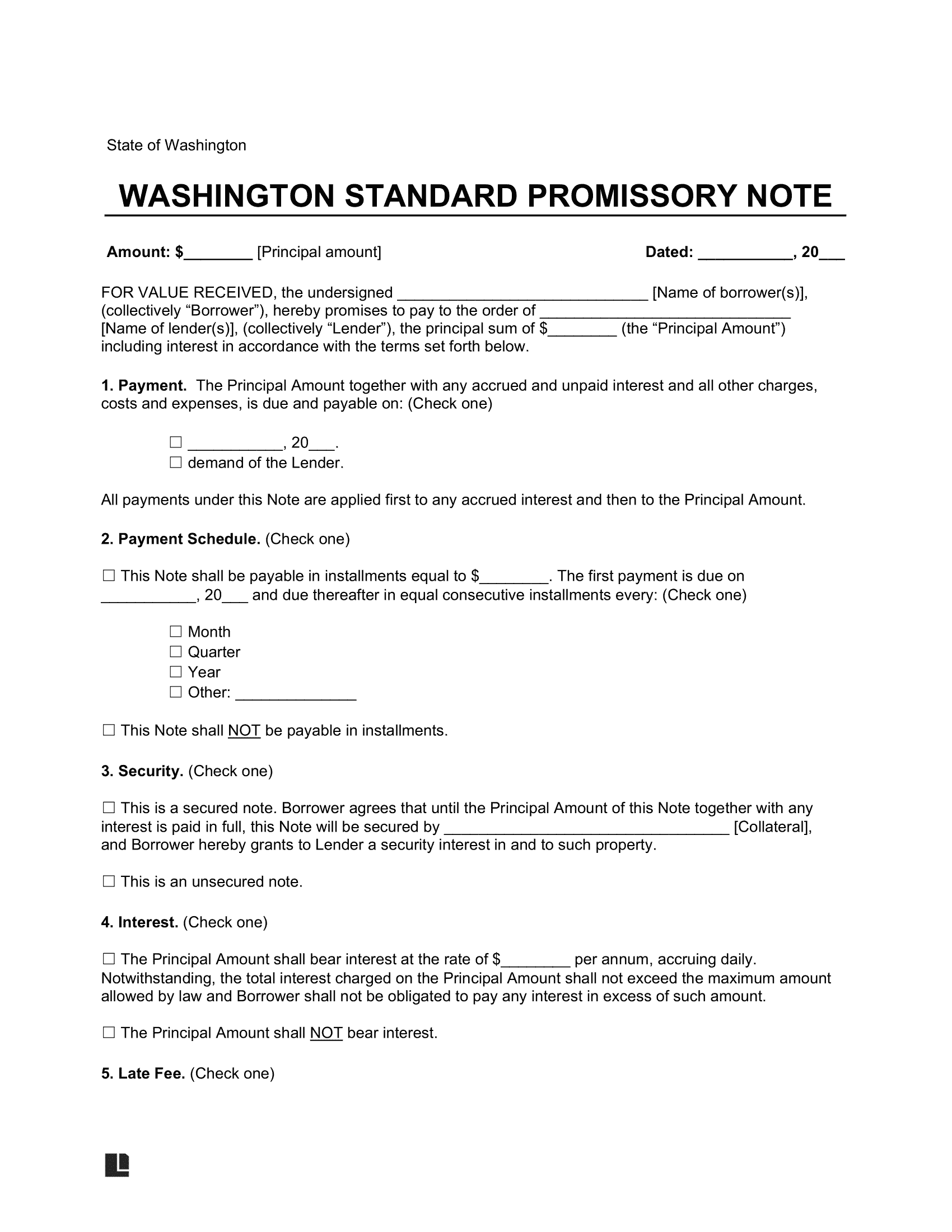

What Is a Washington Promissory Note?

A Washington promissory note is a legal contract that lists the terms of a loan agreement between a borrower and a lender. Lenders often use this document in less formal lending situations, as they commonly use it when loaning to trusted acquaintances, friends, and family members.

It functions as a record of the debt, specifying the initial loan amount, applicable interest rate, repayment schedule, and consequences of late payments. It’s less cumbersome than more elaborate loan documents, ensuring clarity and accountability in personal lending scenarios.

Laws: Title 62a, Article 3 of the Revised Code of Washington covers promissory notes.

Statute of Limitations: Six years (RCW 62A.3-118)(a)).

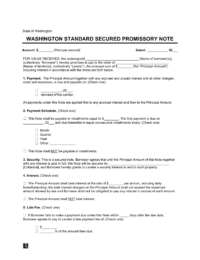

Types of Washington Promissory Notes: Secured vs. Unsecured

Washington lenders and borrowers should match their promissory notes to the loan’s complexity. Whether you need flexibility with an unsecured note or more legal safeguards with a secured one, we help you finalize your note with one of our templates.

Secured Washington Promissory Note

Demands collateral, ensuring the lender receives some of the borrower's property if the borrower fails to repay their loan.

Unsecured Washington Promissory Note

Doesn't involve collateral because of a close relationship between the borrower and lender or proof of the borrower's solid credit.

Usury Laws and Interest Rates

All promissory notes should follow the usury rate regulations in Title 19, Chapter 19.52 (Interest-Usury) of the RCW:

- Without a Contract (§ 19.52.010(1)): 12%.

- With a Contract (§ 19.52.020(1)): 4% over the federal 26-week treasury bill rate or a flat 12% per annum, whichever is greater.

- For Medical Debt Prejudgments (§ 19.52.010(2), § 19.52.020(4)): 9%.

- For Unpaid Consumer Debt Judgments (§ 4.56.110(5)): 9%.

- For Unpaid Student Debt Judgments (§ 4.56.110(4)): 2% over the federal prime rate.

- For Tortious Conduct of an Individual/Entity Judgments (§ 4.56.110(3)(b)): 2% over the federal prime rate.

- For Tortious Conduct of a Public Agency Judgment (§ 4.56.110(3)(a)): 2% over the federal 26-week treasury bill rate.

- For Child Support Judgments (§ 4.56.110(2)): 12%.

- For Judgments with Contracts (§ 4.56.110(1)): The interest rate will be the same as the parties agree to in the contract.

- For Loan Setup Charges (§ 19.52.020(2)(b)): The lender may charge the lesser 4% of the advanced amount or $15.00.

Sample Washington Promissory Note

View a free example of a Washington promissory note to see what it looks like. Using our document editor, create your own and download your copy in PDF or Word format.